Abstract Report - CONSOB AND ITS ACTIVITIES

REPORT 2023

The Report provides evidence on corporate governance of Italian companies with ordinary shares listed on the main Italian regulated market organised and managed by Borsa Italiana Spa, Euronext Milan (EXM).

In particular, the 2023 edition of the Report examines: the ownership structure of listed companies and the evolution of the presence of women on the boards at the end of 2023; the characteristics of corporate boards taken from the corporate governance reports published by firms in 2023 and referring to the 2022 financial year; the results of votes on remuneration policies and remuneration reports in the AGMs held in the first half of 2023 by the 100 largest listed companies by capitalisation (94% of total market value at the end of June 2023); the types of related party transactions disclosed by listed companies to the public and CONSOB in the period 2011-2023.

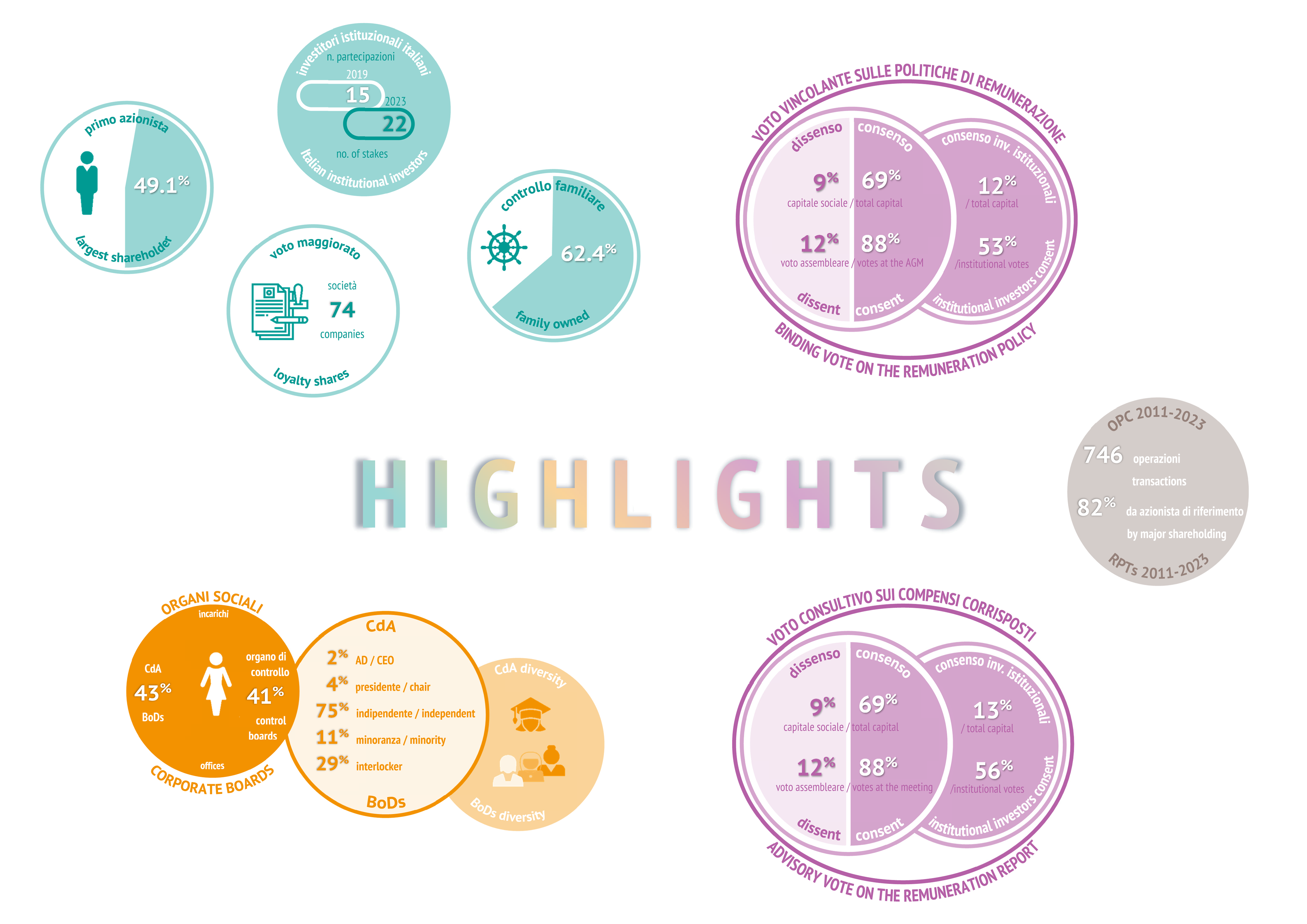

| Ownership and control structure Data on governance of Italian listed companies at the end of 2023 confirm the high ownership concentration and low control contestability of companies. With regard to ownership concentration, the share of the largest shareholder is equal on average to around 49%, in line with the value recorded in 2021 and slightly higher than in 2011. Among relevant shareholders, institutional investors are currently present in 51 companies, down from the 67 investee companies in 2019. The decline is more noticeable for foreign institutional investors (who are major shareholders in 40 companies, down from 55 in 2019). On the other hand, the presence of Italian institutional investors is slightly and gradually increasing (with major stakes held in 17 issuers at the end of 2023, up from 14 in 2019). ... more |

| At the end of 2023, the Italian companies covered by this survey (with ordinary shares listed on the Euronext Milan - EXM) are 210, with a total capitalisation greater than 572 billion euros. The following companies are excluded from the scope of this analysis: those with listed shares other than ordinary shares (one), those with ordinary shares suspended from trading indefinitely (one), and those with registered offices other than Italy, even if the main listing market is in Italy (11). Companies belonging to the financial sector are 43, accounting for 36.6% of the total market value. Firms in the Ftse Mib are 34, as well as those belonging to the Mid Cap; Star firms are 65. Finally, 77 companies are not included in any of the mentioned indices (for further details on the classification adopted, see Methodological notes). The ownership concentration of the Italian listed companies at the end of 2023 is in line with 2021, with the average stake held by the largest shareholder equal to 49.1% (49% in 2021) and that held by the market equal to 38.3% (39% in 2020). The average stake held by the largest shareholder is higher in small firms and in the Mid cap (56.7% in both cases) while is lower in large firms, belonging to the Ftse Mib (where is equal to 29.4%). Families remain the main shareholders in most listed companies, being ultimate controlling agent in 62.4% of the firms, mainly small ones (included in the Star index or not included in any index) and belonging to the industrial sector. State and other local authorities are the controlling shareholder in 11.9% of the cases, mainly large firms in the service sector, while no ultimate controlling agent (UCA) could be identified for almost 18.6% of the issuers, generally large companies operating in the financial sector. Evidence at the end of 2023 confirms the decline in major shareholdings by institutional investors, both in terms of the number of investee listed companies (51 vs. 67 in 2019, with an average stake of around 8%) and as for the number of major shareholding held by such investors (70, 20 stakes down from the amount recorded in 2019). Such a trend is driven by the consistent decline in shareholdings owned by foreign institutional investors, that are major owners of 40 listed companies in 2023, especially large-sized, with a marked decrease from the peak of 55 investee companies recorded in 2019 and a drop of 27 major stakes since then (from 75 in 2019 to 48 in 2023). Italian institutional investors as major shareholders have on the opposite slightly and steadily increased, with 22 stakes in 17 investee listed companies at the end of 2023. At the end of 2023, issuers adopting loyalty shares are 74 (69 in 2021), representing 16.8% of the total market value, more frequently among smaller companies. Seven companies have adopted multiple voting shares (four in 2021). Firms with loyalty and/or multiple voting shares are mainly controlled by families; in these firms the average stake held by the first shareholder is equal to 57.3% (44% in companies that do not envisage this kind of shares). |

| Corporate boards and board diversity As for corporate boards, at the end of 2023 female directors in listed companies peak to 43% of total directorships, being such figure the result of the application of the two-fifths gender quota of the body envisaged by Law no. 160/2019. Consistently with previous years, in three cases out of four (74.9%) women serve as independent directors, while seldom they are the company’s CEO or chairman (respectively, in 20 and 31 cases, equal to 2.3% and 3.6% of women on board). Female board members holding multiple directorships in listed companies (interlocking) regards 28.9% of women at the end of 2023; even if higher than men’s, women interlocking has reduced in recent years, after the peak reached in 2019 (when female interlockers accounted for 34.9% of women directors). The evolution of corporate board diversity over time also reflects the increase in the presence of women on boards due to the provisions on gender quotas; from 2011 to the end of 2022, in particular, there was an increase in the level of education and a diversification of the professional background of directors. The board committees are widespread among Italian listed firms. Over the past five years, in particular, the number of companies establishing a sustainability committee has increased significantly, from 45 companies in 2017 to 123 at the end of 2022 (from 61.3% to 94.5% of capitalisation), given the greater awareness of ESG (environmental, social and governance) issues, which are also expressly referred to in the Corporate Governance Code. ... more |

| The traditional management and control model remains the mostly adopted (98% of the total) by Italian companies with ordinary shares listed on Euronext Milan (EXM) at the end of 2022. Compared to previous years, the size and meetings of corporate boards remain on average unchanged; the weight of independent and minority members continues to slightly increase. In line with evidence on interlocking in recent years, board members holding multiple directorships in listed companies are on average 2 in each company, representing almost one-fifth of the board. Interlockers are present in three companies out of four (163 on 210), which account for 97.5% of total market capitalisation. Interlocking increases with companies’ size, as Ftse Mib firms display on average 3.1 interlockers, representing 26.6% of the board. The proportion of companies carrying out the annual board self-evaluation is also decreasing in 2022 due to the measures of the Corporate Governance Code (CGC), which allow small and concentrated ownership companies to carry out board assessment every three years. By contrast, the number of companies adopting a succession plan remained unchanged, namely 50% of financial firms and around 30% of companies in the non-financial sector in the reference year. The members of the boards of directors (1,948 offices in a total of 202 Italian listed companies at the end of 2022) show attributes in line with previous years: directors are aged on average 57 years, are foreigners in 6% of the board (a share that rises to 12% in the Ftse Mib firms and 21% in companies controlled by financial institutions) and are graduates in about 90% of cases; there is a modest reduction in the managerial background profile (around 64% of cases, falling to less than 60% in the financial sector). The statutory auditors’ profile (628 offices in 202 Italian listed companies as at the end of 2022), although with variations depending on the sector of activity and size of the company as well as the identity of the controlling shareholder, on average shows features similar to previous years: auditors are 57 years old and are foreigners in 1.1% of cases (a share that rises to 2.7% in the Ftse Mib), they are graduates in about 98% of cases (almost exclusively in economic disciplines) and professionals/consultants in 86% of cases (share ranging from 88% in family firms to 76% in companies controlled by financial institutions). Following the application of gender quota regulations, also due to the presence of women on the boards, there has been an increase over the years in the level of education (share of members with a degree and with post-graduate degrees). As regards professional background, the diversification of the boards has increased (in particular, the share of managers has risen from 75% in 2011 to 64% in 2022) while in control boards the predominant role of professionals/consultants is confirmed. In 2022, the remuneration and control and risk committees are present in almost all companies (over 90% of the total), followed by the nomination committee (about 70% of the total) and the sustainability committee (established on average by about 61% of firms, with a share exceeding 90% in publicly controlled companies and in Ftse Mib firms). Also in terms of total capitalisation, the establishment of the mentioned committees in Italian listed companies is very widespread (over 90% on average). Compared to board members characteristics and in line with previous years, the members of the board committees are primarily independent directors (87% of committee members), women in 60% of cases, and directors with a more diversified professional background (less frequent managerial profile, 50%). As a result of gender quotas rules, women representation peaked to the highest values of 43.1% of boards of directors and 41.3% of boards of statutory auditors. In 32 boards of directors (15%) and 51 boards of statutory auditors (24%) the number of women equals or exceeds that of men, being such figures the result of a gradual upward trend in the last three years. Women hold on average 4.1 board seats, with higher values displayed by large and mid-sized companies and financial firms. With a slight increase as compared to previous years, women serve as the company’s CEO in 20, mostly small-sized companies (4.6% of total market value). A woman chairs the board of directors in 31 companies (12.8% of total market capitalisation). In three cases out of four (74.9%) women serve as independent directors and in one case out of ten a woman was appointed by minority shareholders through the slate voting system (91 female directors in 71 large companies, accounting for 77% of total market value). Finally, in line with long-standing evidence, women are more frequently than men interlockers (28.9% of women, versus 20.7% of interlockers in the directors’ entire population). However, after recording the highest value of 34.9% in 2019, women interlocking has in recent years declined and steadied. |

| Annual general meetings The 2023 shareholders' meeting season of the 100 listed companies with the highest capitalisation recorded further growth in shareholder participation: in particular, an average 77.8% of the share capital took part in the AGM, compared to 75.4% in the previous year, setting a new high since 2012 (first year of survey). At the same time, there was a slight decline in the participation of institutional investors, who represented an average of 21.2% of the share capital (21.9% in 2022 and 22.8% in 2021). Specifically, the share of foreign institutional investors amounted to 18.2% of the share capital in 2023 (19.3% in 2022 and 20.4% in 2021), while the share of Italian institutional investors amounted to 3% (2.6% in 2022). The latter took part in 99 AGMs, up from 94 in 2022. In 2023, the shareholders' meeting consent on both remuneration policies, which averaged 68.5% of the share capital, and remuneration reports, which averaged 68.7%, remained virtually unchanged from the previous year. On the other hand, there was a decrease in the number of votes in favour by institutional investors, since, on average, the latter endorsed remuneration policies and remuneration reports with percentages of 52.7 (62.5% in 2022) and 55.7 (67.4% in 2022) of their votes, respectively. ... more |

| In 2023, 68% of Annual General Meetings (AGMs) were held without physical attendance by shareholders (‘closed-door meetings’), who conveyed their proxy votes to a special delegate (Rappresentante Designato), as allowed by the extension until July 31, 2023 of the provisional measures enacted during COVID-19 pandemic, by way of exception to ordinary rules. Remote voting mechanisms, on the other hand, were used in a very small number of cases. By looking specifically at the AGMs of the 100 listed companies with the highest capitalisation, evidence shows an increase in shareholder participation in meetings held in the first half of 2023: an average of 77.8% of the share capital intervened, as compared to 75.4% in the previous year, marking a new peak since 2012 (the first year of the survey). At the same time, there was a slight decline in attendance by institutional investors, representing on average 21.2% of the share capital, as compared to 21.9% in 2022 and 22.8% in 2021. Specifically, the participation of foreign institutional investors amounted to 18.2% of the share capital in 2023, down from 19.3% in 2022 and 20.4% in 2021, while Italian institutional investors accounted for 3% the share capital, slightly up from 2.6% in the previous year. The latter also took part in more meetings, attending 99 out of the 100 sampled AGMs, up from 94 in 2022. Since the 2020 proxy season the vote on the remuneration policy of Italian listed companies has been binding and expressed at least every three years or whenever required following policy changes. During the AGMs held in 2023, 92 companies (out of the 100 listed companies with the highest capitalisation) took a new vote on the remuneration policy and it was approved in all but one case. Considering the votes also cast at the AGMs in previous years by issuers who had defined a policy on a multi-year horizon at that time and therefore did not vote on remuneration policy in 2023, on average participants voted in favour of remuneration policies with a percentage equal to 68.5% of the share capital (67.9% in 2022) and 87.6% of the capital represented at the meeting (89.6 per cent in 2022). Approval of the remuneration policy by institutional investors has decreased over the last year, as votes in favour accounted for 52.7% of the shares owned by such investors (17.1% of the capital represented at the meeting), down from 62.5% in 2022 (20.6% of the capital present at the meeting in 2022). Dissent, which for the purpose of this report includes votes against and abstentions, amounted to 9.2% of the total share capital (up from 7.7% in the previous year) and to 12.3% of the shares represented at the meeting (10.6% in 2022). Most of such dissent can be ascribed to institutional investors, amounting to 8.5% of the share capital (7.2% in the previous year), 11.2% of the votes represented at the meeting (up from 9.9% in 2022) and 47% of total votes cast by institutional investors (up from 37.1% a year earlier). The latter percentage is lower among companies belonging to the Ftse Mib index and the financial sector. With regard to the advisory votes cast on the remuneration report, presenting the compensation paid for the previous year, the votes in favour were nearly 68,7% of the total share capital (virtually unchanged from the previous year) and 87.7% of the shares represented at the meeting, down from 90.8% in 2022. The consent by institutional investors accounted for 55.7% of their votes (17.5% of the capital at the meeting), showing, also in this case, a decline from 67.4% in the previous year (22% of the capital at the meeting in 2022). Institutional investors’ dissent amounted to 8.2% of the share capital, up from 6.1% in 2022. In particular, it increased to 44% of their total votes, up from 32.3% in the previous year; a higher dissent can be found among Mid Cap companies, while a lower percentage is recorded among firms in the financial sector. Overall, dissent was higher on remuneration policy than remuneration report for 48 companies (47, if we consider the dissent of institutional investors out of their total votes), while for 35 issuers (34 in the case of institutional investors) dissent on compensation was higher than dissent on remuneration policy. |

| Related party transactions In relation to material related party transactions (RPTs), in 2011-2023 Italian listed companies carried out 746 transactions (42 in 2023, a figure higher than the previous year, when material RPTs had been 34, but lower than the average figure of 57 documents per year), mostly entered into by smaller companies. Additionally, in 2011-2023, 307 material RPTs have been exempted from CONSOB Regulation being ordinary and at arm's-length conditions (16 in 2023, compared to 27 in 2022 and the average figure of about 24 transactions per year). Such transactions, that have been reported to CONSOB according to the relevant rules, were mainly entered into by larger companies. ... more |

| Over 2011-2023, Italian listed companies entered into 746 material related party transactions (RPTs), issuing a circular according to relevant Italian rules. In 2023 42 RPTs have been reported, being such figure higher than the previous year (34 RPTs) but lower than the average number of 57 documents per year). Material RPTs have been classified according to the tunneling taxonomy developed by Atanasov et al. (2008), based on the nature of the resource transferred to/from the related party, namely asset, cash flow and equity (for further detail, see Methodological notes). Most transactions consist of financing or other contracts (51% of all RPTs since 2011). With a lower frequency, the transactions involve the transfer of major long-term assets (31% of all RPTs) or a rearrangement of the related party’s ownership claims over the firm’s equity, namely by means of mergers or reserved capital increase (18% of all transactions). The related counterparty is in over 4 cases out of 5 (82.3%) the controlling or major shareholder, while in fewer cases the transaction was entered into with subsidiary or associate companies (13%) and non-shareholder directors or key managers or firms affiliated with them (4.7%). In 2011-2023 307 material arm’s length RPTs in the ordinary course of business were reported to CONSOB by Italian listed companies (16 in 2023, lower than 27 RPTs reported in 2022 than the average number of nearly 24 ordinary RPTs reported per year). Most ordinary RPTs were entered into by large companies (included in the Ftse Mib, amounting to 144 RPTs, 47% of the total). Such transactions are mostly part of the operating activities of the reporting listed company (i.e. in 37.8% of cases the supply of typical goods and services by non-financial firms and in 25.4% financing contracts by banks) and were entered into with controlling or major shareholders in 88% of cases. |

The Report was prepared by:

Paola Deriu (coordinator) - CONSOB, Head of Research Department (p.deriu@consob.it)

Angela Ciavarella - CONSOB, Corporate Governance Department (a.ciavarella@consob.it)

Eugenia Della Libera - CONSOB, Research Department (e.dellalibera@consob.it)

Giovanna Di Stefano - CONSOB, Research Department (g.distefano@consob.it)

Lucia Pierantoni - CONSOB, Research Department (l.pierantoni@consob.it)

Rossella Signoretti - CONSOB, Corporate Governance Department (r.signoretti@consob.it)

Elena Frasca - CONSOB, Research Department (e.frasca@consob.it)

The authors wish to thank Giovanni Mollo for his contribution to the definition of the regulatory framework. The opinions expressed in the Report are the authors' personal views and are in no way binding on Consob.

Full text [PDF format]

Time series of data [excel format]

ISSN 2281-535X [online]